MD Tviti od 3.7.2017

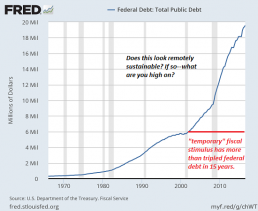

Dolgovi so gonilna sila gospodarstva, ne le slo, tudi svetovnega. Prekomerno se zadolž. države, podjetja in ljudje.

2/Kje so meje? Nihče več ne omenja 60%-BDP za euro-drž. Če gre ZDA čez100%+Japonska čez200%, zakaj ne tudi Kitajska+cel svet! Dolg→potrošnja

3/Dolgovi so lahko enormno visoki dokler so obresti blizu nič+roki vračil vedno daljši ter gospodarstvo+dohodki rastejo. In ko ne kaj potem?

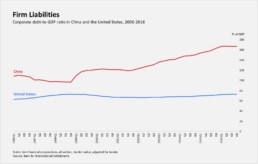

4/SLO ni hitro rastoča kot Kitajska, njen dolg ni pretežno notranji kot Jap/Ital+nima »teže« kot Argentina za100-letni dolg po7,9%_blog-link

Will The Crazy Global Debt Bubble Ever End?

Tyler Durden, Zerohedge May 29, 2017 (Excerpt by MD)

http://www.zerohedge.com/news/2017-05-29/will-crazy-global-debt-bubble-ever-end

Author http://charleshughsmith.blogspot.si/2017/05/will-crazy-global-debt-bubble-ever-end.html

There are multiple sources of friction in the Perpetual Motion Money Machine.

We’ve been playing two games to mask insolvency: one is to pay the costs of rampant debt today by borrowing even more from future earnings, and the second is to create wealth out of thin air via asset bubbles.

The two games are connected: asset bubbles require leverage and credit. Prices for homes, stocks, bonds, bat guano futures, etc. can only be pushed to the stratosphere if buyers have access to credit and can borrow to buy more of the bubbling assets.

If credit dries up, asset bubbles pop: no expansion of debt, no asset bubble.

The problem with these games is the debt-asset bubbles don’t actually expand the collateral (real-world productive value) supporting all the debt. Collateral can be a physical asset like a house, but it can also be the ability to earn money to service debt.

Credit card debt, student loan debt, corporate debt, sovereign debt–all these loans are backed not by physical assets but by the ability to service the debt: earnings or tax revenues.

If a company earns $1 million annually, what’s its stock worth? Whether the market values the company at $1 million or $1 billion, the company’s earnings remain the same.

If a government collects $1 trillion in tax revenues, whether it borrows $1 trillion or $100 trillion, the tax revenues remain the same.

If the collateral supporting the debt doesn’t expand with the debt, the borrower’s ability to service debt becomes increasingly fragile. Consider a household that earns $100,000 annually. If it has $100,000 in debt to service, that is a 1-to-1 ratio of earnings and debt. What happens to the risk of default if the household borrows $1 million? If earnings remain the same, the risk of default rises, as the household has to devote an enormous percentage of its income to debt service. Any reduction in income will trigger default of the $1 million in debt.

If a household earns $100,000 annually, how much can it borrow? The answer depends on the terms of the debt: the rate of interest and the percentage of principal that must be repaid monthly.

If the interest rate is 0% and the monthly payment is fixed at $1, the household can borrow billions of dollars. This is how the game is played: there is no upper limit on debt if the interest rate is effectively zero, or adjusted for inflation, less than zero.

Would you lend the household your savings, knowing you’ll never get any interest and the principal will never be repaid? Of course not. Nobody in a functioning market for capital would throw their hard-earned savings away on a debtor who can’t pay any interest or principal.

The only institutions that can play this game are central banks, which create money out of thin air at zero cost. As for risk–the way to manage defaults is to print more money.

But once again–printing money doesn’t create collateral or income needed to service debt. As I have explained, printing money is akin to adding a zero to currency. Every $1 bill is now a $10 bill. Are you ten times wealthier once the central bank adds a zero to every bill? No, because the $5 loaf of bread is re-set to $50.

The other problem with this game is interest keeps ticking higher while earnings remain flat. Even at very low rates of interest, interest payments keep rising. This is not an issue if income rises along with interest payments, but if income is flat, paying higher interest costs eventually pushes the borrower into default.

The household that borrowed $1 billion at 0% paid no interest. But let’s say the lender now demands 1/10th of 1% interest–nearly zero interest. The household now owes $1 million in annual interest. Oops! Even near-zero interest can generate crushing interest payments once the debt reaches the stratosphere.

The whole game is a bet that future income will rise faster than debt service. Unfortunately, we’ve already lost that bet: household income has been stagnant or declining for years (or for the bottom 90%, for decades), and tax revenues have a nasty habit of falling sharply in recessions and stagnating along with private-sector earnings.

Which leads to the second game: blowing asset bubbles. If the household’s earnings are flat or declining, one magical fix is to inflate the household home’s value from $100,000 to $300,000 in a few years.

Now the household has $200,000 in new wealth it can tap. Wow, was that easy or what? That’s the easiest $200,000 we ever made!

Of course the house didn’t actually gain any additional functional or utility value; it still has the same number of rooms, etc. It still only provides shelter for the same number of residents. The $200,000 in “wealth” that can now be borrowed or accessed via selling the house does not reflect an increase in the collateral’s utility value–it’s all financial magic leveraged off an unchanging utility value and household income.

These games look like a Perpetual Motion Money Machine. There is no cost, it seems, to expanding debt and assets bubbles; if future income doesn’t rise enough to service the growing mountain of debt, we either print more money, lower the interest rate or create “wealth” with even grander asset bubbles.

But there is eventually a problem. At some point, even 0.1% interest becomes unaffordable, and adding zeroes to the currency devalues the currency faster than incomes rise. Asset bubbles run out of greater fools to buy at elevated prices.

Borrowers default, asset prices crash and everyone holding the currency is impoverished.

There are multiple sources of friction in the Perpetual Motion Money Machine. State-cartel inflation eats away at stagnating incomes, rising interest payments eat away at stagnant incomes and tax revenues, and printing money eats away at the purchasing power of the currency. Eventually these sources of friction cause the Perpetual Motion Money Machine to grind to a halt and then shatter.

Put another way, the debt-asset bubble supernova consumes all the available fuel and implodes. I’ve employed the supernova analogy for many years, as it captures the expansion of debt and asset valuations and the resulting collapse once all the fuel in the system (i.e. earnings and real collateral) has been consumed.

Forget Austerity, This Measure Gives Blessing for a Fiscal Fest

Alessandro Speciale, Bloomberg 29.junij 2017 (Excerpt by MD)

https://www.bloomberg.com/news/articles/2017-06-29/forget-austerity-this-measure-gives-blessing-for-a-fiscal-fest

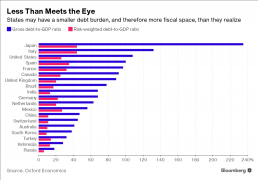

New risk-weighted calculation of sovereign indebtedness shows that there’s plenty of space for government spending

There’s never been a better time to be deep in debt.

A dearth of safe assets, low rates and central bank purchases are keeping bond yields low and are likely to continue doing so for years to come. But governments are missing out on this opportunity to finance investments, partly because of their focus on gross debt-to-GDP ratios.

A new risk-weighted measure of sovereign indebtedness developed by Oxford Economics shows that the burden may be less than governments realize and that there’s plenty of space for more fiscal expansion.

The methodology, steered by Oxford Economics’s head of macro research, Gabriel Sterne, and his colleague, Daghan Ozbilenler, relies on the fact that not all sovereign bondholders are equal: some, like foreign banks and hedge funds, are more likely to take flight when things turn sour and therefore riskier; others, such as domestic pension funds, actually want to avoid destabilizing government finances. At a time when central banks hold large amounts of state debt, this matters.

Graf: https://assets.bwbx.io/images/users/iqjWHBFdfxIU/iHfzjqTIiogk/v0/800x-1.png

“Governments are too concerned about levels of their indebtedness, judging by their inadequate fiscal responses to insufficient demand, inequality and low funding costs,” the authors write. “Although markets may initially react to a major economy’s fiscal expansion by selling long-end government bonds, the subsequent lack of significant inflationary pressures or sustainability issues means that any sell-off would be relatively short-lived.”

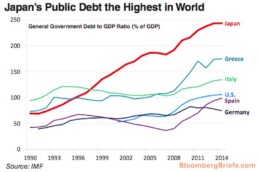

Japan and Italy, with large debt burdens that are mostly held by domestic actors, are the countries that benefit the most from the calculation. But also austerity champions like Germany see a dramatic improvement in recent years, thanks in part to financial retrenchment behind national borders.

In fact, Oxford Economics’s measure can put to rest concerns about the post-crisis expansion of government debt. The risk-weighted debt-to-GDP ratio has risen only 1 percentage point since 2011, compared to the almost 10 percentage points of the gross measure.

There are caveats, however. The main one is that when central banks will eventually start unwinding their balance sheets, the risk-weighted measure will become less favorable. But this is still a long way off everywhere, maybe with the partial exception of the U.S.

One Hundred Years of Indebtedness

Carmen Reinhart, Project Syndficate Lun 30, 2017 (Excerpt by MD) https://www.project-syndicate.org/commentary/argentina-hundred-year-bonds-by-carmen-reinhart-2017-06

In mid-June, the finance ministry (of Argentina) sold $2.75 billion worth of US dollar-denominated bonds that mature in one hundred years. … At the end of the day, this is not about the character of the country, the maturity of the debt, or the size of the issue. It is about the coupon rate on the offering, 7.9%, which is considerably higher than most other plausible alternatives. Just as water finds its level in nature, capital finds its level in international finance: when interest rates are low in core markets, it flows to higher-yielding alternatives.

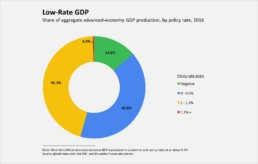

Without question, interest rates are extraordinarily low in advanced economies, pulled down partly by the slowdown in longer-term output growth, but also as a consequence of official efforts. Two of the “big three” central banks, the European Central Bank and the Bank of Japan, have lowered their policy rates into negative territory and continue to add to their balance sheets. As for the third, the US Federal Reserve’s slow motion monetary tightening has just put the federal funds rate above 1%, and plans to pare the Fed’s asset holdings appear to be in the works. As the chart shows, almost one half of GDP in advanced economies is produced where policy rates are below 0.5%. Only a sliver of activity takes place where the policy rate is above 1.5%.

Official measures extend beyond the realm of central banks, too. In terms of the huge stock of foreign exchange reserves held worldwide, the public sector holds more US Treasury securities than the private sector.

These distortions encourage investors in money centers to scan the horizon for more attractive destinations. Argentina got their attention, but so, too, did Cyprus, another country that recently had a financial crisis. Likewise, capital has flowed into Iceland at such a rapid clip that the International Monetary Fund felt obliged to warn that, “overheating risks are a clear and present concern.” … But it’s worth recalling that in the post-1945 period, fully one half of all defaults by emerging-market economies took place at debt-to-income levels below the Maastricht Treaty’s ceiling of 60%. Today, as the waves of market distortions from official policies in advanced economies break on emerging markets’ shores, constructing magical seawalls is not a solution.

Another Lesson from Japan

stephen S. Roach, Project Syndicate Jun 26, 2017 (Excerpt by MD)

https://www.project-syndicate.org/commentary/advanced-economies-low-inflation-weak-demand-by-stephen-s–roach-2017-06

No lesson is more profound than that of a series of policy blunders made by the BoJ. Not only did reckless monetary accommodation set the stage for Japan’s demise; the country’s central bank compounded the problem by taking policy rates to the zero bound (and even lower), embracing quantitative easing, and manipulating long-term interest rates in the hopes of reviving the economy. This has created an unhealthy dependency from which there is no easy exit.

Though Japan’s experience since the early 1990s provides many lessons, the rest of the world has failed miserably at heeding them. Volumes have been written, countless symposiums have been held, and famous promises have been made by the likes of former US Fed chairman Ben Bernanke never to repeat Japan’s mistakes. Yet time and again, other major central banks – especially the Fed and the European Central Bank – have been quick to follow, with equally dire consequences.

From asset bubbles and excess leverage to currency suppression and productivity impairment, Japan’s experience – with lost decades now stretching to a quarter-century – is testament to all that can go wrong in large and wealthy economies. … Japan’s core CPI was basically flat relative to its year-earlier level. For the Bank of Japan (BoJ), which committed an unprecedented arsenal of unconventional policy weapons to arrest a 19-year stretch of 16.5% deflation lasting from 1994 to 2013, this is more than just a rude awakening. It is an embarrassment bordering on defeat.

An inflationless world offers three key insights. First, the relationship between inflation and economic slack – the so-called Phillips curve – has broken down. Courtesy of what the University of Geneva’s Richard Baldwin calls the “second unbundling” of globalization, the world is awash in the excess supply of increasingly fragmented global supply chains. Outsourcing via these supply chains dramatically expands the elasticity of the global supply curve, fundamentally altering the concept of slack in labor and product markets, as well as the pressure such slack might put on inflation.

Second, today’s globalization is inherently asymmetric. For a variety of reasons – hangovers from balance-sheet recessions in Japan and the US, fear-driven precautionary saving in China, and anemic consumption in productivity-constrained Europe – the demand side of most major economies remains severely impaired. Juxtaposed against a backdrop of ever-expanding supply, the resulting imbalance is inherently deflationary.

Third, central banks are all but powerless to cope with the moving target of what can be called a non-stationary liquidity trap. First observed by John Maynard Keynes during the Great Depression of the 1930s, the liquidity trap describes a situation in which policy interest rates, having reached the zero bound, are unable to stimulate chronically deficient aggregate demand.

Sound familiar? The novel twist today is the ever-expanding global supply curve. That makes today’s central banks even more impotent than they were in the 1930s.

Should China Deleverage?

Yu Yongding, Project Syndicate Jun 29, 2017 (Excerpt by MD) https://www.project-syndicate.org/commentary/moodys-downgrade-china-sovereign-debt-rating-by-yu-yongding-2017-06

China’s mounting debt problem recently moved into the spotlight when Moody’s downgraded the country’s sovereign rating. But was the downgrade really warranted?

Though China’s overall debt-to-GDP ratio is not an outlier among emerging-market economies, and its levels of household and government debt are moderate, its corporate debt-to-GDP ratio, at 170%, is the highest in the world, twice as large as that of the United States. China’s corporate leverage (debt-to-equity) ratio is also very high, and rising.

A high and rising debt-to-GDP ratio, which goes hand in hand with a high and rising leverage ratio, can lead to financial crisis through three channels. The first is the deterioration of the quality of financial institutions’ assets, and the decline in the price of those assets. The second channel is refusal by investors, concerned about the rising leverage ratio, to roll over short-term debt. The third way a high debt-to-GDP ratio can lead to crisis is by driving banks and nonbank financial institutions, unable to secure sufficient capital, into bankruptcy.

But none of these scenarios seems like a real risk for China, at least not in the foreseeable future. China is, after all, a highly frugal country, with gross savings totaling 48% of GDP. Moreover, because China’s debt consists overwhelmingly of loans by state-owned banks to state-owned enterprises, depositors and investors feel confident (rightly or wrongly) that their assets carry an implicit government guarantee. And not only is the government’s fiscal position relatively strong; it also has $3 trillion in foreign-exchange reserves – a sum that far exceeds China’s overseas debts.

Still, Moody’s points out, China’s debt-to-GDP ratio is a serious problem. Moreover, to justify its downgrade, it argues that the government’s efforts to maintain robust growth will result in sustained policy stimulus, which will contribute to even higher debt throughout the economy.

But this reading fails to distinguish between the long-term trend of the debt-to-GDP ratio when the economy grows at its potential rate and the real-time debt-to-GDP ratio when the economy grows at a below-potential rate. When an economy is growing at roughly its potential rate, as China’s is today, it makes no sense to lower the growth target below that rate. …(In addition) For years, China has been in the grips of overcapacity-driven deflation. The producer-price index (PPI) has declined in year-on-year terms for 54 consecutive months, while the annual rise in the consumer-price index (CPI) is hovering around 1.5%.

To be sure, China does have reason to implement economic stimulus. The overcapacity that, until recently, dominated the Chinese economy was rooted partly in a lack of aggregate demand (and partly in wasteful overinvestment).

In an ideal world, China’s government could respond by stimulating household consumption. But, in the absence of further reforms in areas like social security, growth in consumer spending is bound to be slow. In the meantime, the government must rely on an expansionary fiscal policy to encourage infrastructure investment, even if it means raising the debt-to-GDP ratio.