MD tviti od 20.5.2017 Posledice bančne apokalipse: regulacija-stresni testi, Basel3-dokapital.,obresti najnižje v 60letih, izguba ugleda http://www.economist.com/news/special-report/21721503-though-effects-financial-crisis-2007-08-are-still-reverberating-banks-are 2/Banke 10let po krizi. Še daleč od uspešnosti pred krizo, vendar bolj odporne pred novo. Ključni so FED/ECB, regulacija, g.rast,ugled+tehn 3/ZDA:EU banke: povezava v kolapsu+razpotje v okrevanju=razlika v hitrosti ukrepov (graf). SLO banke so državne+privat. Prve bi bankrotirale 4/ZDA:EU banke danes=velik razkorak »sanirane«vrednosti (4/+3/ graf). Vredn.NLB=nizka iz istih+dodatnih »slovenskih« razlogov. Prihodnost=?

The Economist May 6th 2017 (Excerpt by MD)

http://www.economist.com/news/special-report/21721503-though-effects-financial-crisis-2007-08-are-still-reverberating-banks-are

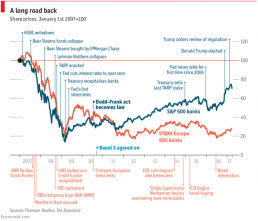

Have the banks at last put the crisis behind them? The STOXX Europe 600 index of bank share prices is still down by two-thirds from the peak it reached ten years ago. European lenders’ returns on equity average just 5.8%.

America’s banks are significantly stronger. In investment banking, they are beating European rivals hollow. Return on tangible equity are expected soon to exceed their cost of capital ( 10%) for the first time since the crisis. But the S&P 500 banks index is still about 30% below the peak it reached in February 2007 (see chart). And the biggest question of all has not gone away: are banks—and taxpayers—now safe enough?

Markets expect the Federal Reserve to raise interest rates after a long pause. That should enable banks to widen the margin between their borrowing and lending rates from 60-year lows. Trump’s victory added an extra boost by promising to lift America’s economic growth rate. He wants to cut taxes on companies, which would fatten banks’ profits directly as well as benefiting their customers. He has also pledged to loosen bank regulation.

Consequences of apocalypse

Ask bankers what has changed most in their industry in the past decade, and top of their list will be regulation. A light touch has been replaced by close oversight, including “stress tests” of banks’ ability to withstand crises, which some see as the biggest change in the banking landscape.

The second big change is far more demanding capital requirements, together with new rules for leverage and liquidity. For too many, leverage was the path first to profit and then to ruin. Revised international rules, known as Basel 3 (still a work in progress), have forced banks to bulk up, adding equity and convertible debt to their balance-sheets.

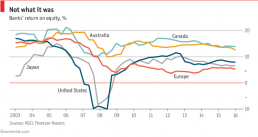

Third, returns on equity have been lower than before the crisis. In part, that is a natural consequence of a bigger equity base. But the fallout from the crisis has also squeezed returns in another way. Central banks first pushed interest rates to ultra-low levels and then followed up with enormous purchases of government bonds and other assets. This was partly intended to help banks, by making funding cheaper and boosting economies. But low rates and flat yield curves compress interest margins and hence profits. The share of cash in American banks’ balance-sheets jumped from 3% before the crisis to a peak of 20% in 2014. As the world economy is at last reviving after several false starts, earnings may pick up in Europe as well as in America.

The financial sector’s reputation was trashed by the crisis. One scandal followed another as the story of the go-go years unfolded: providing mortgages to people who could not afford them; mis-selling securities built upon such loans; selling expensive and often useless payment-protection insurance; fixing Libor, a key interest rate; rigging the foreign-exchange market; and much more.

Financial technology is becoming ever more important. That may be in a highly regulated industry better news for banks than it sounds; with focus on costs, effective use of resources & human capital.