MD tviti od 15.6.2017 Kdo razume današnji svet ali vsaj preteklost? Kdo zna videti prihodnost? Bo tehnologija+Kitajska spremenila svet1/4 http://milandemsar.com/xi-jinpings-marco-polo-strategy/ 2/ %BDP sveta: Evropa je šele pred <200 leti prehitela Kitajsko. ZDA je šele po ww2 prehitela Evropo. Kmalu bodo vsi trije spet izenačeni 3/ Kitajska je samo v zadnjih 10-letih povečala %bdp sveta od 4,5% na 13,4%. Ali: razviti svet 1980=59% - ostali 41% → 2018 1=41% - 2=59% 4/ Hitra Kitajska rast je v upadanju, rast razvitih držav po 8-letih normalna. Vendar ob nenormalni ekološki(Kitajska=30%)+monetarni politiki Teksti v nadaljevanju so povzetki člankov: Xi Jinping’s Marco Polo Strategy A World Turned Inside Out China future stability clouded by the domestic debt bubble

Xi Jinping’s Marco Polo Strategy

Joseph S. Nye, Project Syndicate, Jun 12 2017 (Excerpt by MD)

https://www.project-syndicate.org/commentary/china-belt-and-road-grand-strategy-by-joseph-s–nye-2017-06

Originally announced in 2013, Xi’s plan to integrate Eurasia through a trillion dollars of investment in infrastructure stretching from China to Europe, with extensions to Southeast Asia and East Africa, has been termed China’s new Marshall Plan as well as its bid for a grand strategy.

China’s ambitious initiative would provide badly needed highways, rail lines, pipelines, ports, and power plants in poor countries. It would also encourage Chinese firms to increase their investments in European ports and railways. The “belt” would include a massive network of highways and rail links through Central Asia, and the “road” refers to a series of maritime routes and ports between Asia and Europe.

Reallocation of China’s large foreign-exchange assets away from low-yield US Treasury bonds to higher-yield infrastructure investment makes sense, and creates alternative markets for Chinese goods. With Chinese steel and cement firms suffering from overcapacity, Chinese construction firms will profit from the new investment. And as Chinese manufacturing moves to less accessible provinces, improved infrastructure connections to international markets fits China’s development needs.

But is the BRI more public relations smoke than investment fire? According to the Financial Times, investment in Xi’s initiative declined last year, raising doubts about whether commercial enterprises are as committed as the government. Five trains full of cargo leave Chongqing for Germany every week, but only one full train returns.

Shipping goods overland from China to Europe is still twice as expensive as trade by sea. As the FT puts it, the BRI is “unfortunately less of a practical plan for investment than a broad political vision.” Moreover, there is a danger of debt and unpaid loans from projects that turn out to be economic “white elephants,” and security conflicts could bedevil projects that cross so many sovereign borders. India is not happy to see a greater Chinese presence in the Indian Ocean, and Russia, Turkey, and Iran have their own agendas in Central Asia.

A World Turned Inside Out

Stephen S. Roach, Project Syndicate, Apr 26 2017 (Excerpt by MD)

https://www.project-syndicate.org/commentary/developing-countries-drive-global-growth-by-stephen-s–roach-2017-04

Fully a decade after the Great Financial Crisis, global growth is finally returning to its 3.5% post-1980 trend. But this round trip hardly signals that the world is back to normal.

At the margin, the recent improvement has been concentrated in the advanced economies, where GDP growth is now expected to average 2% over 2017-2018 – a meaningful pick-up from the unprecedentedly anemic 1.1% average growth of the preceding nine years. Relative strength in the United States (2.4%) is expected to be offset by weakness in both Europe (1.7%) and of course Japan (0.9%). However, annual growth in the advanced economies is expected to remain considerably below the longer-term trend of 2.9% recorded during the 1980-2007 period.

By contrast, the developing world keeps chugging along at a much faster pace. Although the average growth rate expected for these economies over 2017-2018, at 4.6%, is about half a percentage point lower than during the preceding nine years, they would still be expanding at more than twice the pace of the developed world. Unsurprisingly (at least to those of us who never bought into the Chinese hard-landing scenario), strength in the developing world is expected to be concentrated in China (6.4%) and India (7.5%), with growth lagging in Latin America (1.5%) and Russia (1.4%).

This persistent divergence between developed and developing economies has now reached a critical point. From 1980 to 2007, the advanced economies accounted for an average of 59% of world GDP (measured in terms of purchasing power parity), whereas the combined share of developing and emerging economies was 41%. That was then. According to the IMF’s latest forecast, those shares will completely reverse by 2018: 41% for the advanced economies and 59% for the developing world.

The pendulum of world economic growth has swung dramatically from the so-called advanced countries to the emerging and developing economies. New? Absolutely. Normal? Not even close. It is a stunning development, one that raises at least three fundamental questions about our understanding of macroeconomics:

First, isn’t it time to rethink the role of monetary policy?

The anemic recovery in the developed world has occurred against the backdrop of the most dramatic monetary easing in history – eight years of policy interest rates near the zero bound and enormous liquidity injections from vastly expanded central-bank balance sheets.

Yet these unconventional policies have had only a limited impact on real economic activity, middle-class jobs, and wages. Instead, the excess liquidity spilled over into financial markets, sustaining upward pressure on asset prices and producing outsize returns for wealthy investors.

Second, has the developing world finally broken free of its long-standing dependence on the developed world?

Growth in global trade slowed to a 3% average pace over the 2008-2016 post-crisis period – half the 6% norm from 1980 to 2016. Yet, over the same period, GDP growth in the developing economies barely skipped a beat. This attests to a developing world that is now far less dependent on the global trade cycle and more reliant on internal demand.

Finally, has China played a disproportionate role in reshaping the world economy?

The export share of Chinese GDP tumbled from 35% in 2007 to 20% in 2015, while its share of global output surged from 11% to 17% during this period. China, the world’s largest exporter, may well be in the vanguard of global decoupling.

China’s tertiary sector (services) has gone from 43% of GDP in 2007 to 52% in 2016, whereas the share of the secondary sector (manufacturing and construction) has fallen from 47% to 40% over the same period.

All of this speaks to a radically different world than that which prevailed prior to the Great Financial Crisis – a world that raises profound questions about the efficacy of monetary policy, development strategies, and the role of China. While some healing of an $80 trillion global economy is now evident, progress needs to be seen through a different lens than used in past cycles.

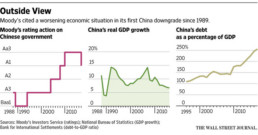

China future stability clouded by the domestic debt bubble

Country Risk Assessment-Credendo, 22 Mar 2017 (Excerpt by MD)

https://www.credendo.com/country_risk_assessment/china/future-stability-clouded-domestic-debt-bubble

Risk drivers and outlook

We are about to see a changeover of the majority of the Chinese Communist Party leadership. However, political continuity will be maintained with Xi Jinping remaining firmly in power at a time of gradual slowdown driven by China’s economic rebalancing. The process is too slow as Beijing continues to support economic growth in order to preserve social stability. However, it also further fuels the rise of an already heavy domestic debt. Therefore, clouds are forming over a country steadily hit by large net capital outflows and a decline in the RMB value and foreign exchange reserves. Nevertheless, those reserves are still at a very high level and allow China to be classified in category 1/7 for short-term political risk.

Faced with external pressures, China has started to tighten some capital controls and raise interest rates. In the future, the Chinese economy will remain under pressure in the context of a strong USD, wide interest gap with the USA, weakened global trade (which could worsen if US President Trump triggers a trade war with China) and adverse domestic developments. The latter mostly concern the corporate debt spiral and the deteriorating health of the banking sector. Beijing has yet to draw up a decisive debt-reduction strategy for mainly state companies, recapitalise the banks and introduce better regulation for shadow banking. China’s two greatest structural risks are primarily domestic – as external debt is low – and to a great extent are mitigated by high household savings, the State’s strong net creditor position, low central government debt and its control on the most important corporate and banking players. Those buffers combined with political stability justify classifying China in category 2/7 for medium- to long-term political risk. Beijing acknowledges the need for reforms and for corporate debt reduction, as witnessed by various measures taken in past years. However, those are largely insufficient given the overwhelming scale of the problem. There are clear doubts about President Xi Jinping using a stronger second mandate to launch bolder reforms, including the restructuring of state companies. Therefore, the longer substantial reforms are delayed, the bigger the risks and consequences of a financial (and economic) crisis and the weaker the State’s capacity to withstand it. In a tricky and uncertain transition context with highly indebted companies, persisting industrial overcapacities and higher payment delays, China continues to be rated in the highest (C/C) commercial risk category.

China’s international weight to gain from potential US isolationism

Facts show that China increasingly contests US political and economic world dominance, a trend that could accelerate in the event of a more isolationist US policy. The modern version of the Silk Road under the “One Belt, One Road” initiative highlights this. Enhanced cooperation with governments in countries where infrastructure projects are planned allows Beijing to record substantial trade and economic benefits while increasing its political weight on the world scene through mutually advantageous relations. China is also actively promoting its role as a financing provider by setting up new international institutions (e.g. AIIB) and as a free trader (e.g. the planned “Regional Comprehensive Economic Partnership”).

Pro-growth policy vs. economic rebalancing

Beijing is expected to reduce stimuli and tighten its monetary policy as domestic pressures have increased in the face of widening imbalances. After a sharp rebound in prices, the government is expected to cool down the overheating property sector by cutting the excessive loans that have contributed to corporate debt rising further to extremely worrying levels.

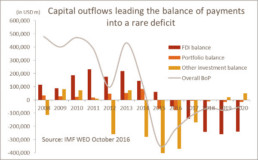

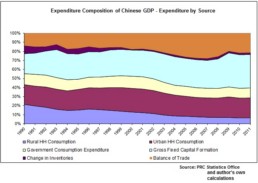

Economic rebalancing is underway as evidenced by the economy’s soft landing, a dominant services sector and steadily strengthening consumer demand. However, government policies don’t really point to a firm commitment to an economic model change. The transition to a consumption-led economy is far too slow, as demonstrated by China’s persistent reliance on domestic investments (still at a high 43.7% of GDP in 2016) and robust – but forecast to decrease – current account surplus. Shaken by a negative trend in net capital flows, the balance of payments has fallen into overwhelmingly negative territory since 2015 and is forecast to remain in deficit in the MLT. It reflects China’s structural developments, notably stronger Chinese FDI fuelled by increasing overseas acquisitions from Chinese groups expanding internationally, and a sustained capital flight since 2014.

Controls tightened to stem capital outflows and RMB decline

Capital outflows brought the RMB down to its lowest level against the USD since 2008 after a 7% drop in 2016. The RMB is now more market-driven and managed against a broader basket of 24 currencies to alleviate market pressure from the USD. However, even though it has appreciated slightly against this basket, the RMB has become more volatile since the surprise 3% devaluation against the USD in August 2015. Several interest rate hikes seem increasingly likely in spite of the negative effect it could have on highly indebted companies.

Corporate debt at alarming levels

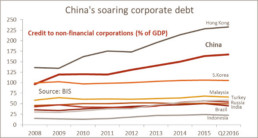

China’s biggest risks continue to grow. The continued deterioration of heavy corporate debt and banks’ bad loans alter the longstanding perception that China will be able to avoid an economic and financial crisis. The current trend of Chinese growth driven by inefficient credit and increasingly requiring debt to sustain high GDP growth is unsustainable. The stock of corporate debt is huge, around 170% of GDP. Beijing is aware of the debt time bomb but keeps delaying the economy’s deleveraging process. Some measures have been taken, such as debt-to-equity swaps, wiping out hundreds of identified zombie companies and launching mergers and acquisitions in the steel and coal sectors.

A banking and financial crisis on the cards

The debt spiral, translated into abundant low-quality bank assets, threatens to trigger a banking and financial crisis if there is no decisive corrective action. In this scenario, companies and banks (and numerous non-banking players) would be hit, negatively spilling over to economic activity beyond 2017.

Beijing’s financial power to withstand domestic shocks

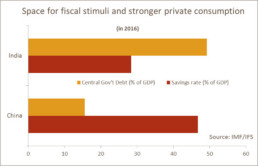

Increasing corporate and banking risks are mitigated by China’s high household savings, strong net international creditor position and low central government debt. The longer Beijing refuses lower economic growth, the less effective existing buffers will be and the more postponing the necessary reforms will weigh on MLT growth potential. Compared to corporate debt, public debt is much more moderate. Thanks to a favourable budget situation and low debt (at 15% of GDP), China’s central government has room for manoeuvre to use fiscal stimuli.

Hence, the country’s budget deficit widened to 3% of GDP last year – which is also roughly forecast in the coming years – whereas general government debt is on an upward trajectory, rising from less than 40% of GDP in 2014 to an expected 50% this year. This trend will continue as the State supports a slowing economy. However, a larger share comes from local governments, whose debt is still growing as they continue to issue off-budget bonds alongside the bond swap initiative launched in 2015.

A low external financial risk

China has low and sustainable external debt, thereby confirming that its debt problem is primarily of a domestic nature. It has even decreased since 2015, from 16.8% of GDP in 2014 to an expected 10.2% of GDP in 2016.

In spite of a high short-term external debt burden, accounting for 78% of total external debt in mid-2016, external liquidity is very strong. Indeed, China has the world’s biggest foreign exchange reserves, covering around 16 months of imports and 3.5 times the short-term external debt. Nevertheless, reserves have dropped, for the first time since 1992, by 21% in 2015/16 as a result of net capital outflows and the PBC’s interventions to limit the RMB’s decline.