MD tviti od 15.5.2017 https://www.project-syndicate.org/commentary/competition-in-the-digital-economy-by-dalia-marin-2017-05 2/ Živčnost je posledica skromnih rezultatov po svet..fin.krizi kljub vložkom 1.000-ev mlrd.$, €, ¥. Trendi preteklega 10-letja so nevzdržni 3/Nemčija 2016-300 mlrd.$ trg.suficita. Je N problem za EU+ZDA? Je preveč varčna+konkurenčna? Naj izstopi iz eura? Gre za suficit zunaj eura

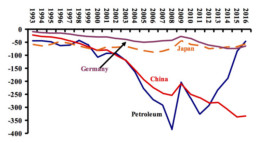

4/ ZDA 2016-500 mlrd.$ trg.deficita; v24-letih s Kit(4)-Jap(2)-Nem(1)=7 tisoč mlrd.$. Graf pove veliko.Manjkajo kapitalski tokovi. ∑+/-ov=?

Barry Eichengreen Project Syndicate May 11, 2017 [Excerpt by MD]

For US President Donald Trump, the measure of a country’s economic strength is its current-account balance – its exports of goods and services minus its imports. This idea is of course the worst kind of economic nonsense. It underpins the doctrine known as mercantilism, which comprises a hoary set of beliefs discredited more than two centuries ago. Mercantilism suggests, among other things, that Germany is the world’s strongest economy, because it has the largest current-account surplus.

In 2016, Germany ran a current-account surplus of roughly €270 billion ($297 billion), or 8.6% of GDP, making it an obvious target of Trump’s ire. [Yet,… as a member of the eurozone, Germany has no exchange rate to manipulate; the European Union has anti-subsidy regulations; it is not that Germany discriminates against imports; it is irrelevant for welfare when countries run surpluses with some trade partners and deficits with others]

Germans collectively spend less than they produce, and the difference necessarily shows up as net exports. Germany has a high savings rate for good reason. Its population is aging more rapidly than most. Its sensible people are sensibly saving for retirement.

This is why the advice that Germany would be better off abandoning the euro and letting its currency appreciate – makes little sense. Changing the exchange rate would not diminish the incentive for Germans to save. The correspondence of savings minus investment with exports minus imports is not an economic theory; it’s an accounting identity.

The question, ultimately, is why Germany should seek to reduce its current-account surplus. IMF thinks that doing so would be good for a world economy in which investment is in short supply, as evidenced by record-low interest rates. It would be good for Southern Europe, which needs to export more, but can only do so if someone else, like the largest Northern European economy, imports more. Most of all, more investment in infrastructure, health, and education would be good for Germany itself. Chancellor Angela Merkel in contrary to Martin Schulz suggests cutting taxes to increase household spending’s and corporate investments.