Extract from the Article: “The $8.9 Trillion Question: What Happens When Central Banks Exit Bond Markets?” by Milan Demšar

Central banks have been the world’s biggest buyers of government bonds and may soon turn into sellers—a tidal shift for global markets. Yet investors can’t agree on what that shift will mean.

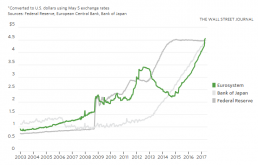

By buying bonds after the 2008 financial crisis, central banks across the developed world sought to push yields lower and drive money into riskier assets, reducing borrowing costs for businesses. Recent data showed that the European Central Bank holds total assets of $4.5 trillion, more than any other central bank ever. The Fed and the Bank of Japan both have $4.4 trillion.

With the world economy finally recovering, investors believe that holdings at the Fed and ECB have peaked. U.S. officials are discussing how to wind down their portfolio, which they have kept constant since 2014. The ECB’s purchases of government and corporate debt are now more likely to be tapered later in the year, analysts say.

So, if the ECB stops its monthly €60 billion ($66 billion) of purchases, it is the weaker government debt and corporate bonds that could be hardest hit.

“Those countries that have weaker macro dynamics, such as larger debt piles, will be affected more strongly,” said Arnab Das, a senior analyst at Invesco. “If it’s not done carefully, at the bare minimum the transition could be extremely disruptive.”

Bonds are stockpiled by banks, which profit by dealing in them. If these banks know they can always sell a large chunk of their stock to the central bank, they are more willing to offer investors a better price for those bonds. Riskier, less liquid assets particularly benefit.

Some investors say that, if QE works, it is mostly as a message from central bankers to markets that they are committed to low rates. If that is correct, then officials can protect markets from a steep selloff even if they sell back bonds, as long as they loudly commit to keeping interest rates low.

Mr. Williams calculates that selling a third of the Fed’s bond portfolio would have roughly the same effect as raising rates to 3% from their current 1% level.

For the ECB, the challenge is to “disentangle the rate expectations from the tapering,” said Bastien Drut, a strategist at French asset manager Amundi.

Many expect bond yields could rise and shares fall, some see little effect at all, while others suggest it is riskier investments, such as corporate bonds or Italian government debt, that will bear the brunt.

The Wall Street Journal May 9 2017