MD tviti od 17.6.2017

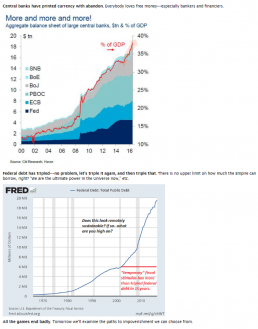

ECB/FED ter BoJ/PBoC so preprečile svetovni fin.+gospodar.kolaps. »Natisnile« so ∞denarja +znižale obresti naO% 1/4 http://milandemsar.com/europes-secret-bailout/

2/ To se v zgodovini še ni zgodilo+ni normalno. Gre za zaupanje v denar brez podlage, ker bo ta morda ustvarjena v prihodnosti. Zato≠vrnitve

3/Trendi so nevzdržni, zato postopna normalizacija, strukturne reforme,… ali pa zlom primerljiv vojni+nov začetek. Svet čaka, ?se bo zgodilo

4/Čez največ 1-leto bo ECB-QE ukinjen+obresti višje. EU-jug bi »we only need time«, ne reforme. Italija s 400mlrd.€bad loans lahko zamaje EU

Teksti v nadaljevanju so povzetki člankov:

Europe’s Secret Bailout

Italy on the Brink

A Broadway Musical’s Lessons for Europe

Will the Fed and U.S. Monetary Policy Ever Get Back to ‘Normal’?

Europe’s Secret Bailout

Hans-Werner Sinn, Project Syndicate Nov 28 2016 (Excerpt by MD)

https://www.project-syndicate.org/commentary/risky-eurozone-debt-buybacks-by-hans-werner-sinn-2016-11

MUNICH – While the world worries about Donald Trump, Brexit, and the flow of refugees from Syria and other war-torn countries, the European Central Bank continues to work persistently and below the public radar on its debt-restructuring plan – also known as quantitative easing (QE) – to ease the burden on over-indebted eurozone countries.

The QE program seems to be symmetrical, because each central bank repurchases its own government debt in proportion to the size of the country. But it does not have a symmetrical effect, because government debt from southern European countries, where the debt binges and current-account deficits of the past occurred, are mostly repurchased abroad.

…

For the Greece, Italy, Portugal and Spain (GIPS) countries, these transactions (the Target debt amounted “close to €1.000 billion”-opp) are a splendid deal. They can exchange interest-bearing government debt with fixed maturities held by private investors for the (currently) non-interest-bearing and never-payable Target book debt of their central banks – institutions that the Maastricht Treaty defines as limited liability companies, because member states do not have to recapitalize them when they are over-indebted.

If a crash occurs and those countries leave the euro, their national central banks are likely to go bankrupt because much of their debt is denominated in euro, whereas their claims against the respective states and the banks will be converted to the new depreciating currency. The Target claims of the remaining euro system will then vanish into thin air, and the Bundesbank and the Dutch central bank will only be able to hope that other surviving central banks participate in their losses. At that time, German and Dutch asset sellers who now hold central bank money will notice that their stocks (Target claims amounted “nearly €1.000”-opp)are claims against their central banks that are no longer covered.

One should not assume that anyone is actively striving for a crash. But, in view of the negotiations – set to begin in 2018 – on a European fiscal union (implying systematic transfers from the EU’s north to its south), it wouldn’t hurt if Germany and the Netherlands knew what would happen if they did not sign a possible treaty. As it stands, they will presumably agree to a fiscal union, if only because it will enable them to hide the expected write-off losses in a European transfer union, rather than disclosing those losses now.

A Broadway Musical’s Lessons for Europe

Mohamed A. El-Erian, 3.jan 2017 (Excerpt by MD)

https://www.bloomberg.com/view/articles/2017-06-08/sweden-figured-out-how-to-stop-people-from-smoking

No matter how hard they try — and they have been trying very hard — the committed central bankers at the ECB cannot produce what Europe needs most for durable economic and financial well-being — that is to say, sustainable high and inclusive growth. No matter how much they experiment and how deep they venture into “unconventional policy,” their tools are fundamentally ill-suited for the task. The well-being of Europe depends on the actions of others.

It requires governments to recognize the fragility of the euro zone’s current policy construction, and for them to do a lot more to improve it — by adopting pro-growth structural reforms, engaging fiscal policy where there is room, granting debt relief where it is urgently needed, and progressing on strengthening the regional economic and financial architecture.

Europe may well need some sort of political surprise, to shock or scare governments out of a damaging mix of paralysis and complacency. Without that, European nations will fail to transition to high inclusive growth and genuine financial stability.

Italy on the Brink

Philippe Legrain, Project Syndicate, Dec 8 2016 (Excerpt by MD) https://www.project-syndicate.org/commentary/italy-referendum-eurozone-by-philippe-legrain-2016-12

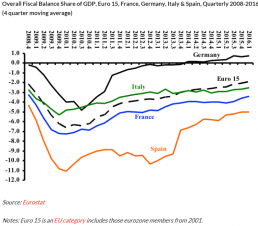

Italy’s economy is no larger today than it was in 2000. And despite the boost from the ECB’s QE program, a weak euro, and the looser fiscal policies of recent years, output is growing at an annual rate of less than 1%. Moreover, Italy could barely stabilize its public debt – which now amounts to 133% of GDP – even when bond yields were reaching record lows. An economic downturn or rising interest rates would thus send public debt soaring again – and Italy cannot count on the ECB to continue buying its bonds indefinitely.

Italy’s political situation – marked by a sense of never-ending misery and growing resentment against the EU and Germany – is equally unsustainable. Youth unemployment is at 37%. Eurozone fiscal rules continue to chafe. Italians used to be enthusiastically pro-European, and saw EU governance as preferable to corrupt domestic mismanagement. But support for the euro, the EU, and the country’s pro-EU establishment has plunged.

The mere possibility of Italy leaving the eurozone – which would entail the redenomination of €2.2 trillion of Italian government bonds in devalued lira – could spark financial panic. It is also implausible that Germany would offer to enter into a eurozone fiscal union that entails pooling its debts with Italy’s.

In addition to stronger demand in the eurozone, Italy desperately needs bold leadership – to restructure its banks, write down unpayable corporate and household debts, reform its economy, boost investment, and clean up its politics. So it is scarcely reassuring that both the eurozone and Italy are likely to try to muddle on for now.

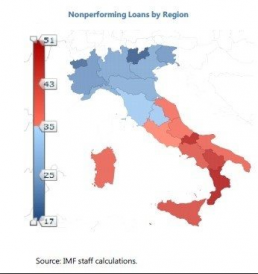

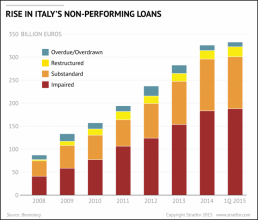

Italy’s Banks – the Elephant in the Room, Knowledge Wharton, Is Europe Headed for…Crisis… “Italy is where they were 20 years ago — they haven’t grown,” says Franklin Allen. About a fifth of Italian banks’ loans — nearly $400 billion — is considered nonperforming, according to a 2015 International Monetary Fund report. The figure accounts for 40% of all troubled loans in the eurozone. “The Italian banking industry could potentially have a huge impact across Europe.”–Franklin Allen

The focus is now on Italy’s largest bank, UniCredit SpA., which is hoping to raise $14 billion in a rights issue and clean up its balance sheet by shedding $19 billion in non-performing loans, bundled into securities to be sold to investors. Some observers say this is potentially the key flashpoint in all of Europe. As “a very big bank with a major subsidiary in Germany,” Allen notes, “the Italian banking industry could potentially have a huge impact across Europe.” That subsidiary, HypoVereinsbank, is one of Germany’s largest banks by total assets.

With Germany’s second-largest bank — Deutsche Bank — struggling as well, it’s possible that the finance world could return to “where we were in 2008,” Allen says. “It’s still not that likely of an outcome, but it’s certainly a significant possibility.” The collapse of one or more Italian banks could trigger troubles elsewhere in the EU, and even affect Germany’s Deutsche Bank, as well as U.S. financial institutions.

Will the Fed and U.S. Monetary Policy Ever Get Back to ‘Normal’?

Knowledge Wharton, May 30 2017 (Excerpt by MD) http://knowledge.wharton.upenn.edu/article/will-fed-u-s-monetary-policy-ever-get-back-normal/?utm_source=kw_newsletter&utm_medium=email&utm_campaign=2017-05-30

In its quest to save the U.S. economy during the financial crisis, the Fed went where it never — gone before. The central bank slashed the target for its key short-term interest rate, to nearly zero and pumped a record $2 trillion into the economy by buying troubled mortgage-backed securities and other assets, ballooning its balance sheet more than four-fold. Now, as the economy seems to be finding solid footing, the Fed is looking to resume historically, pre-Great Recession, normal.

But can it do so, or is this a new normal? … The Fed has, post-2008, become a vastly more complicated place,…Fed is much more than a monetary policymaker, but is also sitting in the big chair for all systemic risk and financial stability regulation and supervision, both before and after financial crises. In that sense, the central bank world before 2008 no longer exists and will never be restored. The [financial] crisis has made sure that the Fed will be a prominent player in economic policymaking for the indefinite future.”

The Fed’s plan to return to normal consists of raising interest rates to pre-Great Recession levels and whittling down its balance sheet, with the pace dependent on U.S. economic performance. There is no general consensus on how the Fed should unwind its balance sheet, although several members of the FOMC have suggested that they would like to see this occur throughout 2017 and 2018. We are, as we have been, in a tentative space that depends on an uncertain future.

Moving too quickly could undo much of what the economy has already accomplished. Rushing back into “a world where the Fed has a less than $1 trillion balance sheet, with interest rates in the 3% to 4% range, could deal a serious blow to the fragile, if not very long, economic recovery.

The ECB is looking to end its own quantitative easing program as green shoots appear in EU economies. Europe is doing much better than last year, and the year before. You see growth pretty much everywhere. The jobless rate has been falling across the board, even in troubled economies such as Italy, Spain and Portugal. Overall, the picture is very positive so QE is going to be done in Europe. We’ll start seeing pressure for higher interest rates next year and maybe even this year.

Shabbir expects to see a readjustment globally, as well as “a degree of turmoil,” including the potential for a “disruptive capital flight” from developing nations. “The currencies of the developing countries may experience elevated volatility with a weakening trend against the dollar, which may increase the dollar-denominated as well as the domestic country debt — sovereign as well as corporate — of these countries, increasing their vulnerability to economic shocks.”

The U.S. growth has been slow, but at the same time, we have seen huge advances in automation technology, spurred by artificial intelligence and machine learning, etc.. While overall output growth has been slow, firms have been adopting new technologies, as evidenced by the rapid growth in the deployment of industrial robots, for example. Eventually, this has to manifest itself in rising productivity. The danger is that technological transformation will cause a massive disruption in the labor markets as U.S. workers are slow to acquire new skills.”