MD tviti od 4.7.2017 »Panta rei« - vse teče, vse se spreminja. Prehitro ali prepočasi, na bolje/slabše, odvisno od nas/od drugih 2/Ni nove ekonomike, stara se nadgrajuje. Bilateralizem ni nadomestilo za multilateralizem. Trendi monetarne politike + ekologije so nevzdržni! 3/Globalizacija=bila prehitra, vendar=bilateralizem morda boljši za ZDA. Euro=problem, vendar=izstop morda boljši za Italijo. =SLO v dilemi? 4/Znanost, tudi ekonomska=ne-dodelana, vendar alternative ni. EU več hitrosti=rešitev za euro-konvergenco + bolj socialni EU-jug _ blog-link

Economics in Transition

Diane Coyle, Project Syndicate Jun 23, 2017 (Excerpt by MD) https://www.project-syndicate.org/onpoint/economics-in-transition-by-diane-coyle-2017-06

The University of Manchester’s Diane Coyle reviews three recent books assessing what has and hasn’t changed in economic thinking and research since the 2008 crisis. Andrew Lo, Adaptive Markets: Financial Evolution at the Speed of Thought, Princeton University Press Richard Bookstaber, The End of Theory: Financial Crises, the Failure of Economics, and the Sweep of Human Interaction, Princeton University Press Roderick Floud, Santhi Hejeebu, and David Mitch, eds., Humanism Challenges Materialism in Economics and Economic History, University of Chicago Press

Since the 2008 global financial crisis, there has been no shortage of criticism of conventional economics, with its rigid models and fanciful “representative agents,” which utterly failed to predict the collapse. But the critics often overlook the emergence of new approaches – some predating the crisis – that could redefine the mainstream of economic thinking. …Not that everything about the state of economics is fine; far from it. But only if today’s critics of economics pay more attention to what economists are actually doing will they be able to make a meaningful contribution to assessing the state of the discipline.

A Royal Doubt

Ten years on from the financial crisis of 2007-2008, two of the most recent books criticizing economics and economists start with the question posed by Queen Elizabeth II on a 2008 visit to the London School of Economics: “Why did nobody see it coming?” (Indeed, almost all the recent examples of this literary genre start the same way.) …Yes, economics needs to change, but it is changing – and has been since some time before the financial crisis.

To be fair, the introduction to Humanism Challenges Materialism acknowledges this: “Economics has taken on a much more behavioral turn,” the editors point out, and “something deeper is stirring.” The essays offer a range of perspectives on the work of McCloskey, long a dissident in economics for her insistence on the importance of values and norms in economic development, and on the role of rhetoric in economics itself. McCloskey mocks what she calls “Max U” economics, which reduces individual humans to nothing more than maximizers of utility or profit.

The point – that many economists ignore the fact that markets are a social phenomenon – is reasonable (but it doesn’t mean she’s Austrian School economist vs neoliberal Chicago fundamentalist). …Within economics, interest in history and the role of culture and institutions has been growing for the past 20 or 30 years. It is now positively fashionable terrain.

History Ignored

Macroeconomic models in wide use before the 2008 crisis excluded financial institutions and relied on the fiction of “representative agents.” This is changing all too slowly. The field is full of normative terminology, about “optimal” outcomes, for instance, without ever analyzing the implied value judgments. …Macroeconomic modeling ignores the fact that economic time series are non-ergodic (a technical way of saying that their characteristic behavior can be completely different in different contexts or periods). History matters.

But The End of Theory goes on to charge that economics has ignored behavioral psychology. In fact, behavioral economics is one of the most popular areas of the discipline now, among academics and students alike. Bookstaber also asserts that economists ignore the reality of complexity theory, network theory, and agent-based modeling. While these latter areas are not mainstream, they, too, are increasingly popular among younger academics. …(Farther) Agent-based modeling involves computer simulations of economies made up of many individual “agents” behaving according to different specified rules or “heuristics.” The model is given a set of starting values, and in each time period the many individual agents react to their new environment. In agent-based models, in contrast to the traditional kind, financial crises can happen.

The Mind of the Market

Andrew Lo’s Adaptive Markets is a masterly synthesis of the traditional, rationality-based approach and new approaches based on psychology and neuroscience, evolutionary theory, and techniques such as computer simulations and artificial intelligence.

One of the most effective points made by advocates of Fama’s now-notorious Efficient Markets Hypothesis is that it is in fact difficult to beat the market; profit-making opportunities are swiftly arbitraged away. And, indeed, Lo argues that when financial markets are stable enough for long enough, the rationality-based model is appropriate. But the moment there is any instability, human fear, greed, culture, behavioral norms, storytelling, and imagination kick in. The environment determines the way market participants behave.

As the title hints, Adaptive Markets sets economic behavior firmly in the context of the human sciences. Lo insists that economic theory must be consistent with evolutionary biology and neuroscience.

Redefining Mainstream Economics

Behavioral psychology, complexity theory, agent-based modeling and the like, along with historical narratives, an emphasis on institutions, methods such as randomized control trials and now big data and AI, are by no means a coherent new mainstream.

Practicing economists outside universities do not keep up with the research frontier – although even here, useful tools such as behavioral economics, complexity theory, market design, and network theory are making significant inroads. Still, the economics taught in university departments, practiced in financial firms, and applied by policymakers remains heavily reliant on old-fashioned reductionist rational-choice models.

Does Addressing Bilateral Trade Imbalances Work?

Martin Feldstein, Project Syndicate Jun 27, 2017 (Excerpt by MD)

https://www.project-syndicate.org/commentary/trump-addressing-bilateral-trade-deficits-by-martin-feldstein-2017-06

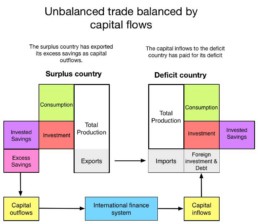

Politicians and economists view trade imbalances very differently. Consider the United States’ trade deficit. Economists emphasize that the total US trade deficit with the rest of the world is the result of policies and actions at home. Simply put, if the US invests more than the country as a whole saves, it must import the difference from the rest of the world, creating the existing trade deficit.

But politicians (and the general public) tend to focus on bilateral trade deficits with individual countries, like the $300 billion imbalance between the US and China. They blame the bilateral deficit on Chinese policies that block imports of US products and subsidize Chinese exports to the US.

Economists explain that those policies affect the composition of the US trade imbalance, but not its size. If China changed its trade policies in ways that reduced the bilateral deficit, the US trade deficit with some other country would increase, or its surplus with some other country would shrink. The overall US trade deficit with the world, however, would not change.

Economists also like to stress that free trade raises a country’s overall income. There are winners and losers, but the winners from free trade could in principle compensate the losers by enough to make everyone better off. Economists don’t talk very much about such compensation, because governments don’t do much to arrange it for the losers.

The US has policies like the Trade Adjustment Assistance program, which provides more generous unemployment benefits for workers who lose their jobs because of competition from imports. But the federal government doesn’t provide such assistance on a large scale, presumably because it makes no effort to provide compensation to those who lose their jobs because of technological change. And rightly so.

Imports cause losses to particular industries, occupations, and geographic areas. And those who lose – or stand to lose – from imports demand protectionist measures, in the form of tariffs or quotas, against those specific products. Adam Smith recognized this even before David Ricardo explained the virtue of free trade.

We saw this response explicitly in US President Donald Trump’s election campaign, during which he threatened to impose high tariffs on products from China, Mexico, and other countries.

But now that he is president, those high tariffs or quotas are nowhere to be seen. Instead, we see trade negotiations being conducted under the threat of such tariffs – and leading to market opening for some products and services in countries with which the US has a bilateral deficit.

…

The bottom line is that bilateral trade imbalances are not irrelevant and can be useful in directing attention to policies that reduce the real incomes of consumers and businesses. But remedying those bilateral imbalances has to be approached with caution.

Signals on Stimulus Roil Global Markets

The Wall Street Journal, June 28 2017 (Excerpt by MD)

https://www.wsj.com/articles/signals-on-stimulus-roil-global-markets-1498691765

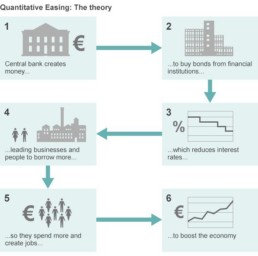

Easy money unleashed by global central banks is receding, a development that could test a range of assets—from stocks to real estate—that have become tightly linked to monetary support since the global financial crisis.

When and how much Western central banks pull back from their unprecedented run of ultralow interest rates and large-scale asset purchase programs, known as quantitative easing, are the foremost questions for global investors.

The prospect of an end to stimulus has lurked in the background for months but has zoomed to the fore now that signs of an economic recovery are beginning to appear in regions, especially Europe, that have struggled to shake off the aftereffects of the global financial crisis.

An end to the ECB’s bond buying “is probably the most important supply-demand change that we can foresee in bond markets. Global bond markets have been strongly interconnected, and U.S. government bonds closely tracked moves in Europe on Wednesday. The yield on the 10-year Treasury note rose to 2.223%. Higher yields on European government bonds make U.S. government bonds less attractive to overseas investors, who have been buying up Treasurys in search of better returns than what they can get at home.

Investors had been selling government bonds and buying the euro since Tuesday, when ECB President Mario Draghi’s comments, delivered at an ECB conference in Sintra, Portugal, on a “strengthening and broadening” economic recovery were interpreted as a sign the central bank was preparing to trim its massive bond buying.

Officials at the Fed, the ECB and BOE are actively debating whether they might be withdrawing support too soon, or too late.

Mr. Draghi’s remarks follow a run of strong eurozone economic data this year. Growth has firmed, unemployment has fallen, and business and consumer confidence is at highs not seen since before the financial crisis. Lending to households in the eurozone grew at a faster pace in May while lending to firms held steady, the ECB reported Wednesday.

This is the Fed’s calculation, too. With the U.S. jobless rate down to 4.3%, the Fed is expected to raise short-term rates one more time this year and start shrinking its bond portfolio.

Some government officials in Europe are growing concerned about the side effects of years of easy money. In Germany, Europe’s largest economy, senior officials have complained for years that low interest rates harm savers and pensioners. The nation’s central bank has warned that house prices may be overvalued by as much as 30%.

Not all central banks are ready to shift toward tighter policy. Bank of Japan officials have emphasized that, with inflation still far below its 2% target, they will stick with its current mix of stimulus efforts, including negative interest rates and asset purchases.

Weidmann Meets the People With Reassurances on ECB Policy Path

Bloomberg, 1.julij 2017 (Excerpt by MD)

https://www.bloomberg.com/news/articles/2017-07-01/weidmann-meets-the-people-with-reassurances-on-ecb-policy-path

German savers critical of the European Central Bank’s ultra-loose monetary stance have received some words of reassurance from the head of their own monetary institution.

Normalization will “hopefully happen, and that’s something we’re working on and discussing,” Bundesbank President Jens Weidmann told a public audience at the institution’s Frankfurt headquarters on Saturday. “We are coming out of the worst economic crisis in post-war history, and therefore expansive monetary policy is appropriate. We just shouldn’t hold onto this policy for longer than necessary.”

As the ECB tries to judge how the euro-area economy would fare if monetary stimulus is pared back, Germany remains one of the biggest critics of the 2.3 trillion-euro ($2.6 trillion) bond-buying program and negative interest rates. Weidmann: “I can certainly understand the frustration a lot of people have who want to save their money.”

A key challenge facing the ECB, according to Weidmann, is that normalizing ultra-loose monetary policy might pose difficulties in countries that didn’t use the period of low borrowing costs to restructure their finances and push through economic reforms. Stimulus shouldn’t be kept ultra loose for longer than is necessary in order to accommodate these member states, he said.

Looking Through

It’s also important that officials look through temporary effects on price growth in order to determine whether their goal has been reached, he said. With the economic recovery in the euro area appearing to solidify, policy makers will need to decide how much of the acceleration in inflation is demand-driven, and how much is being driven by factors like energy prices.

“The discussion isn’t so easy,” Weidmann said, acknowledging the economy’s robust growth but adding that the primary mandate is inflation, which remains lackluster. “We are in complete agreement within the ECB Governing Council that expansive monetary policy remains appropriate and it’s clear we won’t completely throw on the brakes. What we do discuss — and controversially so — is how expansive it should be.”

Lokomotive Theory

Weidmann answered one question about whether having the ECB even made sense, considering the heterogeneity of the euro area, by invoking the memory of former German chancellor Helmut Kohl, who died in June. “When the union was founded there was an intense political discussion about how a currency union works,” he said. “Helmut Kohl was certainly one of the people who stood for a so-called locomotive theory — first we form the union and the rest will come. The Bundesbank leaned more toward the coronation theory that a currency union needs a certain degree of convergence.”

How Monte dei Paschi Ended Up on the Verge of Nationalization

Giovanni Legorano, The Wall Street Journal July 3, 2017 (Excerpt by MD)

https://www.wsj.com/articles/howmonte-dei-paschi-ended-up-on-the-verge-of-nationalization-1499074200

In the financial crisis, the U.S. government intervened quickly and aggressively to shore up teetering banks and exited with a profit. By contrast, governments in the U.K., Ireland, Spain, and Portugal are still owners of important banks that they’ve rescued over the last nine years, as political pressure, lackluster growth and a failure to restore precrisis levels of profitability stall the process of selling.

Between 2008 and 2013, the U.S. government intervened in some 1,400 banks, while the Europeans stepped in with nearly 500 troubled lenders, according to Mediobanca SpA. The U.S. shut down nearly 500 banks, according to the Federal Deposit Insurance Corp., while the Europeans wound down just a handful.

Time hasn’t made things easier. While the U.S. government exited its stakes after just a few years, Europe didn’t—and has faced low interest rates, a dive in profits and seismic events such as Brexit that have made it harder to sell.

“Banks aren’t today what they used to be five or 10 years ago,” said Filippo Aloatti, Hermès Credit senior analyst in London. “Interest rates are low, capital requirements went up, and lots of regulations mean very little appetite to buy banks.”

In Rome, government and Bank of Italy officials say, choices are driven by a determination to avoid applying Europe’s tough new banking rules, particularly the bail-in clause that demands that shareholders, creditors and even some depositors suffer losses before governments can inject money in struggling banks.

“The situation at Monte dei Paschi has been neglected for years, but if you don’t act quickly problems mount,” said Silvia Merler. Rome lent Monte dei Paschi, the country’s biggest lender, €4.1 billion between 2011 and 2013. Last year the government spent months attempting a private-sector fix, to no avail. During that time the bill rose from €5 billion to nearly €9 billion.

Last month, two banks the fund attempted to rescue last year—Banca Popolare di Vicenza SpA and Veneto Banca SpA—finally went bust, requiring a government rescue. Rome avoided applying the bail-in rules. It instead used bankruptcy laws to liquidate the lenders’ bad assets and sold the good ones to Intesa Sanpaolo SpA for one euro. Rome will give Intesa €5 billion to digest and restructure the two banks and has earmarked another €12 billion in guarantees covering the potential cost of disposing the bad loans and some legal risks

“It was a necessary and unavoidable operation,” said Fabio Panetta, Deputy Governor of the Bank of Italy. In general, Italian officials argue their efforts to limit bail-ins ultimately avoided destabilizing situations that would have carried far higher costs to the sector and, possibly, to taxpayers. “We have always tried to avoid [full] bail in,” says Mr. Panetta.

Europe’s Gradualist Fallacy

Yanis Varoufakis, Project Syndicate Jun 27, 2017 (Excerpt by MD) https://www.project-syndicate.org/commentary/european-integration-based-on-simulated-federation-by-yanis-varoufakis-2017-06

ATHENS – Europe is at the mercy of a common currency that not only was unnecessary for European integration, but that is actually undermining the European Union itself. So what should be done about a currency without a state to back it – or about the 19 European states without a currency that they control?

The logical answer is either to dismantle the euro or to provide it with the federal state it needs. The problem is that the first solution would be hugely costly, while the second is not feasible in a political climate favoring the re-nationalization of sovereignty.

Macron’s idea is to move beyond idle optimism by gaining German consent to turn the eurozone into a state-like entity – a federation-lite. In exchange for making French labor markets more Germanic, as well as reining in France’s budget deficit, Germany is being asked to agree in principle to a common budget, a common finance ministry, and a eurozone parliament to provide democratic legitimacy.

Macron knows that such a federation would be macroeconomically insignificant, given the depth of the debt, banking, investment, and poverty crisis unfolding across the eurozone. But, in the spirit of the EU’s traditional gradualism, he thinks that such a move would be politically momentous and a decisive step toward a meaningful federation.

If I am right that Macron’s gradualism and his federation-lite will prove to be a failure foretold, what is the alternative? My answer is straightforward: Re-deploy existing European institutions to simulate a functioning federation in the four realms where the euro crisis is evolving: public debt, banking, investment, and social deprivation.

Four new initiatives requiring no treaty change or new institution. First, the EIB will embark on a large-scale green investment-led recovery program to the tune of 5% of eurozone income, funded entirely through issues of EIB bonds, which the ECB will purchase in secondary markets, if necessary, to keep their yields ultra-low.

Second, the ECB will service (without buying) the Maastricht-compliant part (60% of GDP) of maturing eurozone sovereign bonds, by issuing its own ECB bonds. These bonds are to be redeemed by the member state whose debt has been partly serviced by the ECB at the very low yields that the ECB can secure.

Third, failing banks will be de-nationalized. Based on an informal intergovernmental agreement, the ECB’s banking supervisor will appoint a new board of directors, and any recapitalization will be funded directly by the European Stability Mechanism. In exchange, the ESM will keep banks’ shares, in order to sell them back to the private sector at some future date.

Fourth, all profits from the ECB’s bond purchases, along with any profits from its internal Target2 accounting system, will fund a eurozone-wide, US-style food-stamp program that provides for the basic nutritional needs of European families falling below some poverty threshold.

EU – Fateful Year 2017

Judith Vorbach on 29 June 2017; Social Europe (Excerpt by MD) https://www.socialeurope.eu/2017/06/eu-fateful-year-2017/

Economic policy has predominantly been run on neoliberal lines, notably since the 1970s. This trend has manifested itself in the liberalization of markets, cuts in public investment, de-regulation, privatization and marginalization of trade unions. The credo runs: The less government interferes in the market and the more it improves the framework conditions for companies (aka supply side), the better for the economy. Growth should then slowly percolate down to the least privileged people (“trickle-down-effect”). The results have fallen way short of expectations – and turned out to be quite the opposite!

The Limits of Globalization Within global competition some countries manage to export more than they import. However, Keynes argued some time ago that this could only happen at the expense of other countries. The assumption that market liberalization leads to economic growth is also questionable, as declining wages come alongside constantly reduced global demand. Whereas within traditional governance structures the role and influence of the state, business and workforce were held in comparative equilibrium, the balance of power has shifted in favor of global corporations. They are free to choose the most favorable location, for example, where they expect short-term advantages because of weak workers´ rights. Some highly mobile international investors confront and take on billions of working people.

The weakness of the European Union The European Parliament as the only democratically legitimized EU institution has of course co-decision powers, but less governmental competence compared to the European Council or Commission, which is the only European institution empowered to initiate legislation.

In addition, the scale of corporate lobbying at EU level is massive. There is also a disparity between economic and political integration. While economic integration in the EU is quickly implemented in an autocratic way by competition decisions of the European Commission and via the case law of the European Court of Justice, political integration requires the approval of all 28 (27) member states in the European Council. To restore the necessary balance between economic and social integration, there are two options: Either reduce the economic ties, or endorse political unification. Obviously, the second option is more promising given globalization.

Right wing populism as an answer to failed anti-crisis policy Governments of EU member states often convey the notion that certain things cannot be changed as they are bound under European or international law or treaties. This uncertainty as to where competence lies leads to a feeling of powerlessness among citizens and facilitates the rise of right-wing movements, which reclaim the capacity to act and sort out problems. …Germany in particular is said to be in control of the EU’s entire economic policy.

Moreover, the “rescue packages” have generated the feeling that European citizens of economically stronger states “have to pay” for those living in economically weaker countries. All this has an increasingly negative impact on the enthusiasm for European integration.

Fateful Year 2017 – what will happen to the EU? Neither holding on to neoliberalism, nor renationalization, nor cosmetic reforms, nor individual measures are the correct answers to the current crisis. Proposed a package of necessary measures: * Transnational democracy * Fair distribution and positive economic growth by joint investments and fight against tax fraud * Liberal economic governance and austerity policy of the Stability and Growth Pact must be immediately terminated. Social rights must take priority over internal market freedoms. * Finally, the reshaping and stabilization of the financial sector is a must.